The Fed's Impossible Position

The Fed's Impossible Position

They can't stop stagflation, and they can't prop up stocks forever

“It’s a hurricane. Right now, it’s kind of sunny, things are doing fine, everyone thinks the Fed can handle this,”

“That hurricane is right out there, down the road, coming our way. We don’t know if it’s a minor one or Superstorm Sandy. You better brace yourself.”

JP Morgan CEO Jamie Dimon spooked markets with those remarks yesterday.

It’s not often I agree with Mr. Dimon, but his comment “everyone thinks the Fed can handle this”, and the implied “but” is perfect.

Jamie Dimon knows the Federal Reserve well. From 2007 to 2012 Jamie served as a Class A Director on the NY Fed’s BoD (FYI, it’s “normal” for bank CEOs to sit on the boards of their regulators). During that period, of course, he also ran JP Morgan.

As the CEO of a megabank, Dimon is intimately familiar with the state of the US economy. On that note, he says JP Morgan will be far more conservative with their lending going forward.

Dimon almost certainly knows that the Fed, and broader economy, can’t handle this witch’s brew:

125% US federal debt/gdp

8.3% official inflation (~15% via ShadowStats 1980 CPI model)

6-15% annual deficit/gdp

Sanctions, embargoes, other supply chain disruptions

Food and commodity shortages

A green transition

As I often note, the Fed can’t raise interest rates much more without risking a collapse in stocks and housing. But crashing asset prices may be the only thing that would actually help tame inflation.

Problem is, if asset prices crash (they haven’t yet), consumer spending would plummet. And that’s 70% of our economy. The resulting drop in consumption would put further pressure on equities, cause a ton of bankruptcies, and have all sorts of other nasty short-term consequences. That would be the very outcome that the Fed has worked so very diligently to prevent since 2008.

Essentially, the Fed is performing a highwire act with no net, while being pelted with paintballs and taser darts.

Higher Rates = Unpayable Debt

One of the elephants in the room is if the Fed raises interest rates to 4 or 5%, the cost of interest on federal debt would quickly balloon to $1T, $2T, and from there a monetization spiral would likely ensue. We’ve got to print more new money to pay for the interest on the old money, and so on.

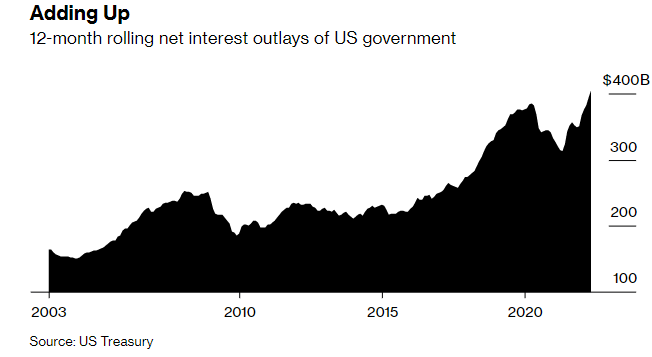

The chart below shows US govt net interest outlays (annual cost of servicing the interest on US debt), via Bloomberg:

That remarkable recent spike from $320B to $400B is worse than it looks in the chart. That’s a 12-month rolling measure, which smooths the impact of rising yields.

More from Bloomberg:

Ten-year Treasury yields have climbed close to 3%, double what they were at the end of last year. Back in July, when the CBO issued its last forecast, it didn’t expect yields to reach that kind of level until around 2027. The rate on every other maturity has soared too, with 3-month bills reaching 1.04% after trading close to zero throughout last year.

The average maturity on US govt debt is currently 6 years. So over the next 6 years, the US will essentially have to roll over 100% of its $32 trillion in public debt. If the yield on that new debt is 6% vs. the 1.5% it was six months ago, that’s going to be a major problem.

And that’s not to mention the incredible strain that higher rates will put on heavily-indebted corporations and households. This economy can’t take interest rates that are anywhere near normal levels. But we can’t comfortably endure the inflation either.

Way I see it, Fed and Treasury are stuck in the greatest financial pickle in history. Today 60% of Americans are living paycheck to paycheck. And an eye-gouging 36% of households making over $250k a year are living paycheck to paycheck! Americans are ill-prepared for a middling gust of wind, let alone the hurricane Dimon predicts.

I continue to believe the Fed will eventually reverse course and be forced to launch GigaQE, taking rates back to zero. It’s still the path of least resistance.

But will stock markets continue to see the same boost effect we have for the last 13 years, now that profit margins are peaking and inflation is raging?

I’m skeptical, and expect very low real (after inflation) returns for US stocks going forward. However, there will be bright spots. Oil and gas seem very likely to outperform, as do value stocks vs. growth. There will likely be nice opportunities to buy these and emerging market stocks during market disruptions.

Don’t Bet on the Fed Long-Term

One more thing about Dimon’s comment that “everyone thinks the Fed can handle this”. Most people I’ve talked with are of this opinion. They’re buying the dip, assuming a Fed rescue is imminent and will be successful. Despite stocks still being expensive, and the economy hurtling towards stagflation and recession.

A few weeks CNBC’s Jim Cramer advised investors to buy the dip, because “It’ll be too late if you wait for the Fed”. Hmm.

To be clear, buying the dip has worked spectacularly well for a long time. As has “don’t fight the Fed”:

But out-of-control inflation is a wildcard the US market hasn’t dealt with in 40 years. Very few traders from back then are even around today.

Even if stock prices keep rising from here, they may not keep up with inflation. But prices could fall another 40% and still not be cheap… To me, the S&P 500 offers a suspect risk/reward ratio.

Stagflation = Buy Gold and Silver

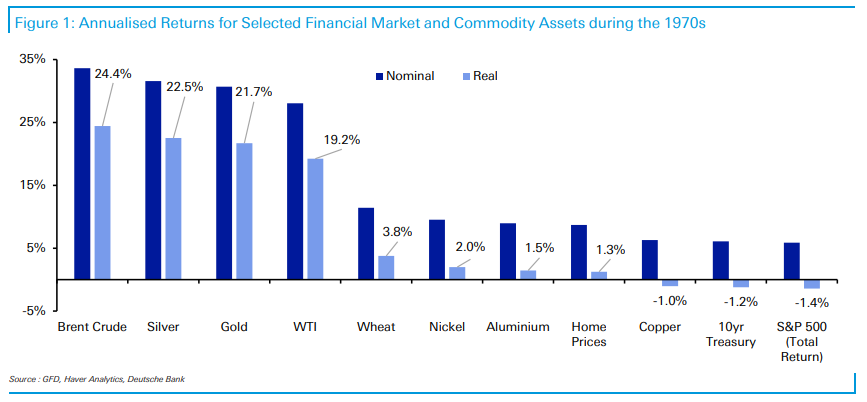

Well, what performs well during stagflation? This chart shows annual returns of various asset classes throughout the 1970s.

Gold and silver averaged 21% and 22% real return a year, respectively, for a decade. Just incredible outperformance. As you can see, in real terms, stocks and bonds performed dismally, with negative real returns compounded over a decade.

The lesson we should learn from the 1970s is straightforward: buy and hold gold and silver during stagflation. I think it applies clearly today. Don’t try to time it. Buy physical metal if possible, or one of Sprott’s physical ETFs (PHYS, PSLV). I don’t recommend GLD, as that is basically “paper gold”.

It may sound crazy, but I think a 25%+ allocation to precious metals is completely reasonable today. I expect to have an oversized chunk of PMs for at least 5 years.

Eventually the time will come to shift from metals and BTC into stocks and startups/venture (this worked quite well in the late 1970s). But I don’t expect to do so until PMs have multiplied in price at least a few times, and equity valuations have fallen by 70% or so in real terms.

I’ll write more about this concept of “timing the long-term asset rotation” in an upcoming piece. It’s important to have a plan (with some flexibility) going into times like these.

Adam